There are certain topics that cannot be ignored at the moment. Environmental protection, climate protection, CO2 values, sustainability, carbon footprint... These are all buzzwords that have been wafting through the press, politics, society and even companies for years... You are measured by how environmentally damaging or, better, how environmentally protective you behave, whether privately or in business. And this applies to all areas of life - nature, fellow human beings, how you run your company and what positive influence you exert on all these areas. As a company, however, you are subject to particular scrutiny, as a large number of laws and regulations need to be complied with. We want to show you what these are, where they come from and how you can have a positive impact even with supposedly small measures.

Content:

ESG – the measure of all behaviour

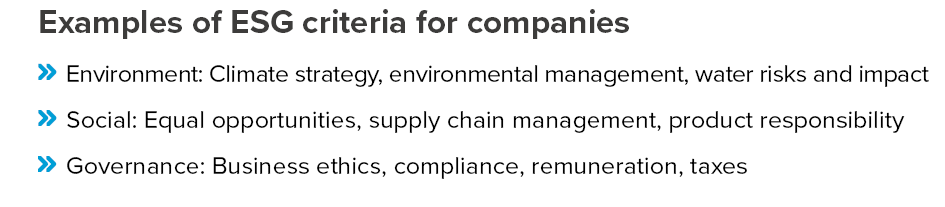

The basis for sustainable action in terms of ESG is the three pillars of environment, social and governance, which were introduced as a term and first concept by the United Nations Global Compact Initiative back in 2004. Over the years, laws and regulations were developed that made the ESG criteria increasingly binding and were intended to provide analysts and stakeholders with measurable values to evaluate companies not only on the basis of their balance sheets, but also in terms of their environmental awareness. Corporate social responsibility (CSR) was already established in many companies and the new laws from 2017 also made it mandatory to publish a sustainability report, which should provide information on non-financial aspects such as environmental concerns, employee concerns, social concerns, human rights and the fight against corruption and bribery. However, not only the company itself, but also its products and business activities are measured against these criteria.

The Green Deal - a good deal?

In 2019, the EU adopted the European Green Deal and launched a comprehensive programme in which it agreed to make the EU climate-neutral by 2050, promote sustainable business practices and embed sustainability in companies. A series of laws and regulations must be complied with and, depending on the size of the company, accountability must be provided in comprehensive ESG and sustainability reports, because the EU believes that "trust is good, control is better".

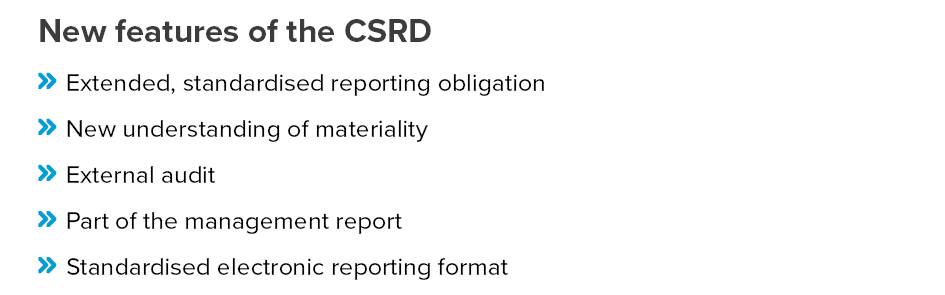

The Corporate Sustainability Reporting Directive (CSRD), which obliges large companies to report on the consideration and handling of social and environmental challenges, was adopted by the EU Parliament in November 2022. The CSRD was intended to expand and strengthen the existing mandatory reporting on non-financial information (Non-Financial Reporting Directive - NFRD). The aim is to provide stakeholders with reliable and, above all, comparable sustainability information so that they can also assess companies according to the values and goals enshrined in the Green Deal.

In an international comparison, the EU is even more comprehensive in its ESG communication than other countries: It not only addresses climate issues, but also topics such as water, pollution, biodiversity and the circular economy. In addition, social aspects and occupational health and safety are addressed and the role of governance, risk and compliance is also focussed on.

The revised directive came into force at EU level in January 2023 and in Germany in January 2024. This gives sustainability information the same status as a company's financial information. But that's not all, because just like the "plain" figures, ESG and sustainability reports should also form an integral part of a company's annual financial statements and be audited by auditors. The new EU standards for sustainability reporting (European Sustainability Reporting Standards - ESRS) must be adhered to.

Who is subject to the (reporting) obligation?

Even before the new directive, around 11,600 companies in Europe were obliged to report on environmental protection, social responsibility, treatment of employees, respect for human rights, combating corruption and bribery and diversity at all levels in the management report or in a separate report as part of the Non-Financial Reporting Directive (NFRD). Recognised national or international report variants were used, but these did not yet meet a uniform standard and were not subject to mandatory auditing. This has changed since January 2024. Since the beginning of the year, around 49,000 companies in the European Union have had to report on the extent to which they act sustainably, in every respect. The reporting is divided into general information, such as business model, strategy, objectives, sustainable corporate governance, due diligence and risk management, as well as topic-specific information such as environmental (including EU taxonomy), social, governance and sector-specific standards. The new EU standards for sustainability reporting (ESRS) must be followed to ensure that the reports are verifiable and comparable.

While the companies previously subject to reporting requirements were all defined as large, listed companies, the group has now been drastically expanded. From the introduction of the new directive, companies that fulfil two of the following criteria are also required to report: They have more than 250 employees, over 40 million euros in turnover or the balance sheet number exceeds 20 million euros.

However, small and medium-sized enterprises (SMEs) can also be subject to reporting requirements, provided they are listed on the stock exchange and are not considered micro-entities. A non-European parent company is no longer an exception, as companies that have achieved a total group turnover of more than 150 million euros in the EU in two consecutive years must now also report.

What are the benefits of the new reporting for companies?

In addition to the overarching goal of making the European Union climate-neutral by 2050, ESG reporting also has direct benefits for companies. Nowadays, no company can avoid the issue of sustainability. Everyone must take action to protect our environment for future generations. This is why ESG now also plays a not insignificant role on the financial floor. Investors no longer just look at turnover, balance sheets and dividends, but also at how environmentally friendly a company is positioned.

The new reporting structure creates greater transparency on the capital market and gives investors a better insight into how their money is being used for the three pillars of sustainability. At the same time, the information requirements of the financial markets and stakeholders are taken into account, thereby creating advantages over the competition. This automatically increases the importance of sustainability strategies within the company and puts them centre stage.

Internal measures have an external impact

However, ESG values should not only be practised externally, but above all internally, because only then is the company credible. Otherwise, you could quickly fall under suspicion of "greenwashing", which would quickly come to light thanks to the new guidelines.

An important component is how the company treats its own employees, how it values them and looks after their well-being. The range of possibilities is broad. It starts with the physical environment. What is the working atmosphere like, how are the offices designed, are they clean, is attention paid to hygiene? The pandemic has brought our health into focus as a valuable asset in recent years. Employees also define the value of their company by valuing their own health and therefore also safety within the company. Is attention being paid to hygiene, is everything being done to keep me healthy? Even today, this can still be a bottle of disinfectant in the toilet or long-term hygiene measures such as antimicrobial coatings on work equipment at the workplace and in public areas of a company. The main transmission route for germs of all kinds is still our hands, because hand hygiene is back to pre-corona levels.

Surfaces in public areas that are frequently touched by many different people can therefore still pose a health risk. After the pandemic is before the pandemic and happy are those who have taken precautions. This can take the form of a permanent antimicrobial coating on banisters in stairwells, door handles or desks and keyboards, for example with TiTANO or the continuous disinfection of escalator handrails with our UVC disinfection module ESCALITE. This disinfection measure not only reduces the risk of infection, but also increases safety, as escalator users can hold on to the handrail without worrying.

These are all measures that can also have a positive impact on the "Social" area, which includes occupational health and safety, or "Governance", which is about employees, in the corresponding ESG reporting.

Conclusion

The new ESG guidelines present companies with major changes and challenges, as ESG requirements must be incorporated into management processes and reporting. Data, processes and management guidelines (governance) must be adapted and reorganised accordingly. However, a holistic view of the company must be taken and even supposedly smaller measures should be included in the evaluation and reporting.

If you are interested in TiTANO or ESCALITE, please contact our sales team.

References:

Comments